Published: Oct 10, 2024

AI everywhere, skin deep

Artificial intelligence (AI) has rapidly evolved from a theoretical concept into a ubiquitous technology that touches nearly every industry and aspect of our life. However, despite its pervasiveness in conversation and its potential to revolutionise businesses, AI’s integration into operations is superficial. The reality is that while AI appears to be everywhere, its impact, depth of integration, and economic benefits are still emerging and unevenly distributed.

This article provides an updated perspective on AI technology trends and state of AI adoption.

Technology trends: the current landscape

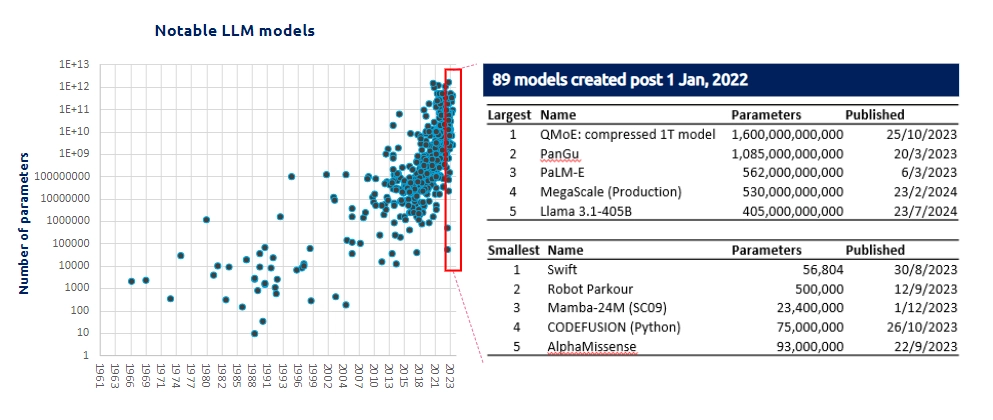

1. Size is not everything

The early wave of AI advancements focused on developing large, general-purpose models, such as the initial large language models (LLMs). These frontier models are becoming increasingly powerful, now incorporating multimodal capabilities that allow them to process and generate both text and images. However, as these models grow in size and complexity, they also bring significant sustainability challenges. The vast amounts of energy required to train and deploy these massive models result in substantial carbon footprints, raising concerns about their long-term environmental impact. GPT-3 which has 175 billion parameters is estimated to have produced ~550 metric tons of CO₂ equivalent emissions (Stanford Institute for Human-Centered Artificial Intelligence (HAI), 2023). To put it in perspective, this amount of CO₂ is roughly equivalent to flying from Singapore to New York USA and back 140 times.

In response to these challenges, a parallel movement is gaining traction, emphasising the development of smaller, task-specific models (Figure 1). These models are designed to perform well on specific tasks with greater efficiency, consuming far less energy and reducing environmental impact. Despite their smaller size, these models often rival larger ones in their respective domains, demonstrating that in AI, bigger isn’t always better. The shift towards more sustainable, use-case-driven solutions highlights a growing recognition of the need for AI to be both powerful and environmentally responsible.

Figure 1: Notable AI models by timeline and the number of weights or trainable parameters. (Epoch AI, n.d.)

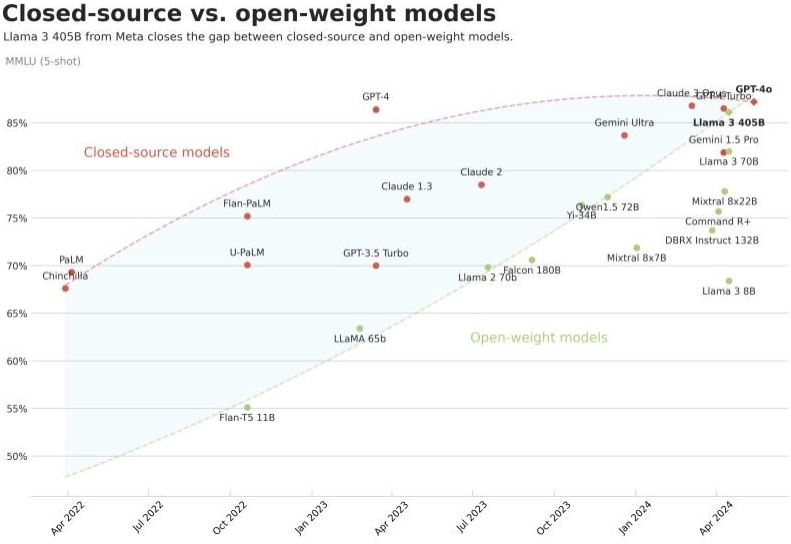

2. The AI fork: open vs. closed

A significant shift in AI technology is the rise of open models, which are publicly accessible through open-source, open-weight parameters or both, enabling broader use and further development by community. These open models are increasingly rivalling proprietary, closed models.

Historically, major tech companies developed and dominated the AI landscape with their proprietary models, limiting access to the most advanced capabilities. However, the emergence of powerful open-source models is democratising access to cutting-edge AI, enabling a broader range of organisations to leverage AI technologies. Figure 2 shows how open-weight models, particularly with the release of Llama3.1 in July 2024, are closing the gap with closed-source ones.

These open models offer cost advantages and foster innovation through community-driven development. As more businesses and researchers contribute to these models, they rapidly improve in performance and usability. The growing adoption of open-source models represents a significant shift in how AI technologies are developed and deployed. We can expect more open models challenging the dominance of closed, proprietary systems and offering new opportunities for businesses to innovate.

Figure 2: Open-weight models closing the gap with closed models (Labonne, 2024)

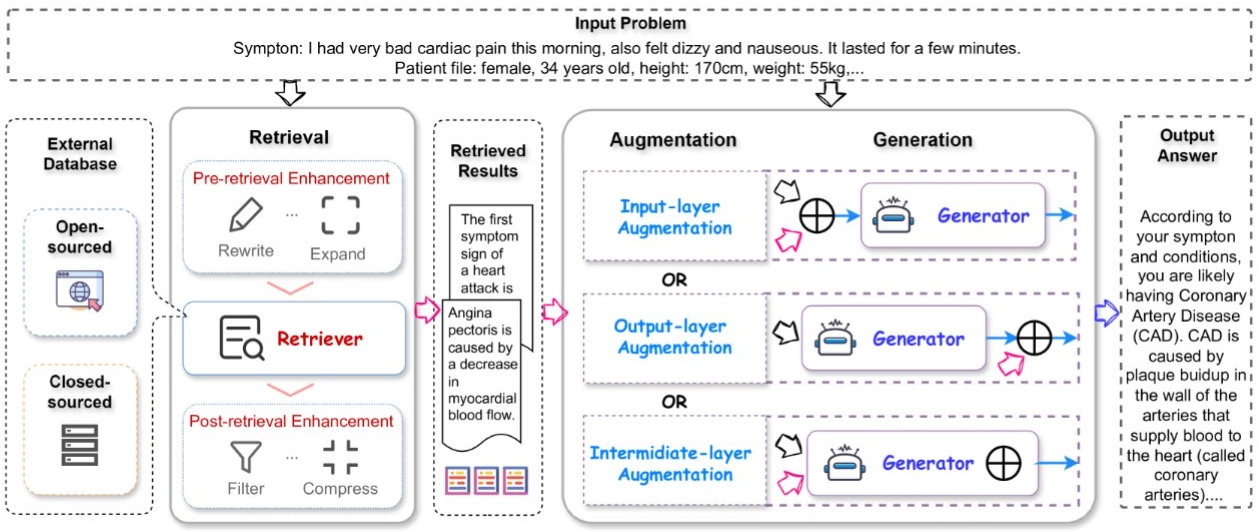

3. From RAG to riches

Retrieval augmented generation (RAG) has emerged as a cornerstone of enterprise use of Generative AI. As shown in Figure 3, RAG combines retrieval-based systems where information is pulled from the organisation’s database of existing knowledge, with Generative AI models that create new content based on that information. This hybrid approach ensures that the risks of AI model “hallucination” are reduced and that the AI outputs are not only accurate but also contextually relevant, providing tailored insights for business decisions. As businesses increasingly rely on AI, RAG enhances the quality and reliability of AI applications, underscoring the need for sophisticated data management and well-structured strategies to unlock AI’s full potential.

In the near future, we can anticipate a significant increase in tools and services leveraging RAG to enable enterprises to effectively mine their proprietary and third-party data using Generative AI. RAG is likely to be viewed as a more accessible and cost-effective alternative to fine-tuning LLMs.

Figure 3. The basic retrieval augmented large language models (RA-LLMs) framework for a specific QA task (Ding, et al., 2024). RAG is continuing to evolve rapidly around 4 areas, namely (1) the RAG Framework/Pipeline, which integrates retrieval mechanisms with generative models to boost the accuracy and relevance of AI-generated outputs; (2) RAG Learning, focused on optimising the interaction between retrieval and generative components through strategic training; (3) Retriever Learning, which involves fine-tuning algorithms to accurately identify and retrieve relevant information from databases; and (4) Pre-/Post-Retrieval Techniques, employed to refine the quality of retrieved data and enhance its effectiveness in generating precise and contextually appropriate AI outputs.

4. From Automation to Autonomy

With the rise of LLMs, LLM-based AI agents have also trended strongly in 2024. AI agents promise a new frontier in which the AI systems are designed to not only analyse data and make recommendations but to autonomously execute actions within defined parameters. Unlike conventional AI, which typically requires human oversight for critical decision-making, agentic AI models are engineered to be capable of reasoning, planning and tool calling which allow them to independently pursue objectives and respond dynamically to new data in real-time environments.

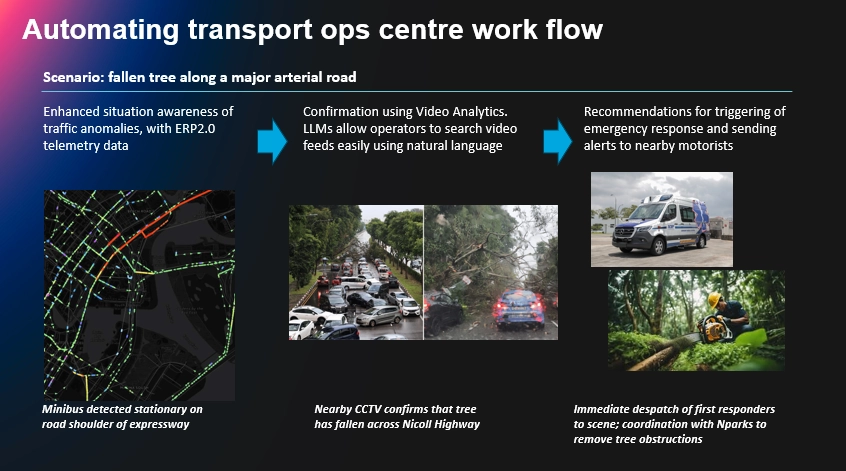

Recent advancements in agentic AI have introduced more adaptive and flexible systems capable of handling complex, multi-step tasks that mimic human autonomy. These advances are starting to transform how organisations can deploy AI, particularly in sectors like transport and logistics, customer service and finance, where rapid decision-making is essential. An example of agentic AI in action is within the Road Transport Operations Centre, whereby agentic AI monitors road traffic conditions using CCTVs and other road infrastructure sensors as well as car-bound telemetry sources, detects anomalies (such as traffic build-up due to road accidents) and automatically activates a set of defined protocols in response to the anomalies (e.g., alerting the first responders and other emergency agencies) with minimal human intervention.

However, the rise of agentic AI also raises unique ethical and regulatory challenges. The capacity for autonomous decision-making introduces potential risks, from unintended actions to biases in the agent’s learning process. As organizations consider agentic AI, robust governance frameworks will be essential to prevent undesirable outcomes.

Looking forward, agentic AI is poised to extend beyond rule-based, pre-programmed behaviors to more adaptable, goal-driven operations, paving the way for next-generation applications across industries. The evolving landscape of agentic AI signals not only an advancement in automation but a shift towards AI that can proactively shape its own processes and deliver more efficient, tailored solutions with minimal human guidance.

Figure 4. Agentic AI can automate responses to unexpected traffic incidents, like a fallen tree blocking a major road. By integrating real-time telemetry data, video analytics, and natural language search capabilities, the system enables rapid confirmation of incidents and coordinated emergency responses. From identifying stationary vehicles to dispatching first responders and alerting nearby motorists, agentic AI streamlines the workflow, reducing response times and enhancing road safety. The faster response enabled by agentic AI will save lives.

Ecosystem shifts: the influence of giants and the local context

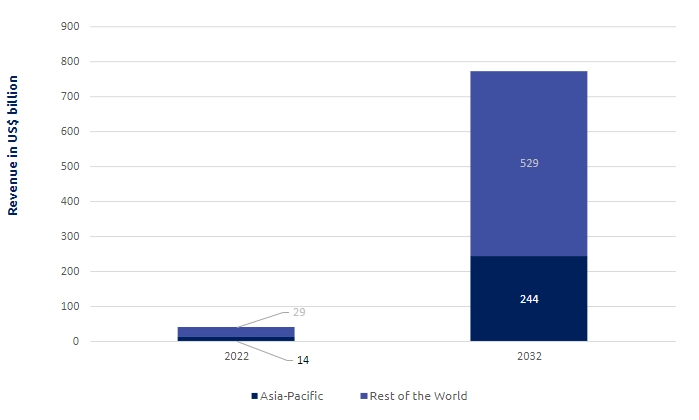

5. Bottleneck in GPUs: giants lead the race

With a market share north of 85%, NVIDIA is the most dominant AI hardware vendor, providing the advanced computing chips or GPUs crucial for training and deploying the LLMs and other foundation models. In 2023, Microsoft and Meta emerged as significant buyers of NVIDIA’s H100 GPUs, spending $9 billion combined and acquiring around 150,000 chips each. Additionally, Google and Amazon purchased approximately 50,000 chips each. Tesla, another large customer, bought 15,000 chips, with plans to increase this number significantly. These figures highlight the substantial investments by these tech giants in AI infrastructure, contributing nearly 40% of NVIDIA’s revenue (Tremayne-Pengelly, 2024).

The rapid adoption of AI by the tech giants has created a bottleneck in the supply of GPUs. These giants have the resources to secure these components, leaving smaller players struggling to keep up. Analysts are predicting the GPU market will grow at a CAGR of 34% over the next decade (Figure 5). With the current industry dynamic, it will not be surprising that this growth be accompanied by an increasingly uneven playing field where only the most resourceful companies can thrive.

Figure 5. GPU market size in 2022-2032 (Precedence Research, 2023)

6. Localsation: tailoring AI to local markets

Localisation is becoming increasingly important in AI deployment. To be truly effective, AI systems must consider the specific needs and conditions of local markets. This has led to the rise of new AI players who offer industry-focused solutions tailored to local contexts, providing businesses with more choices in navigating AI adoption.

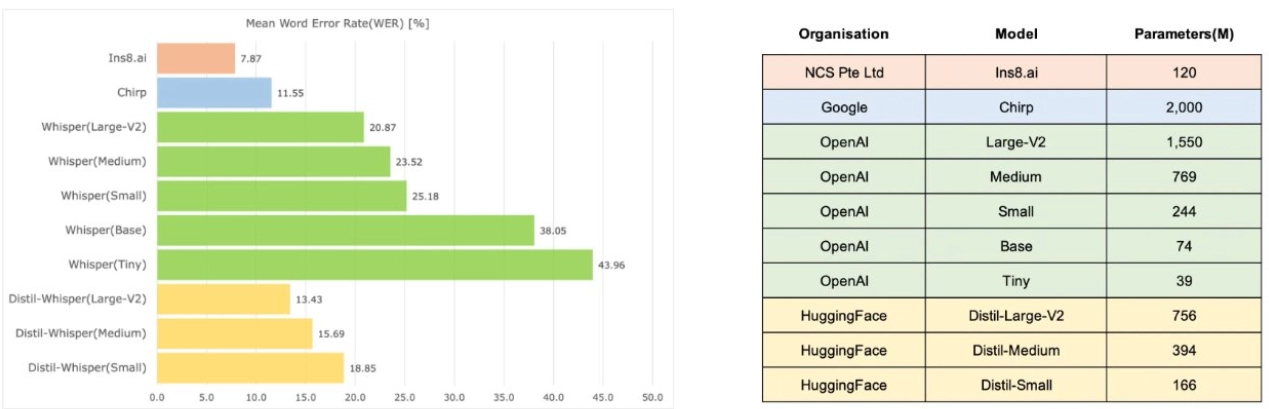

Figure 5 shows the ongoing work that is done by NCS to build a conversational AI system that could understand the Singaporean-accented speech with its use of borrowed words from other languages and many references to local places and events. It is an example of how localisation can improve the performance of AI systems.

Figure 6. Relative performance of AI systems for speech-to-text (STT) transcription of Singlish. Most globally trending STT engines (such as those from OpenAI and Google) are not optimised for understanding languages and their dialects spoken by small populations and communities. AI models trained with local datasets can perform better with fewer parameters and smaller computational footprint, as this example of Ins8.ai by NCS demonstrates.

7. Global AI landscape: not all that glitters is Western

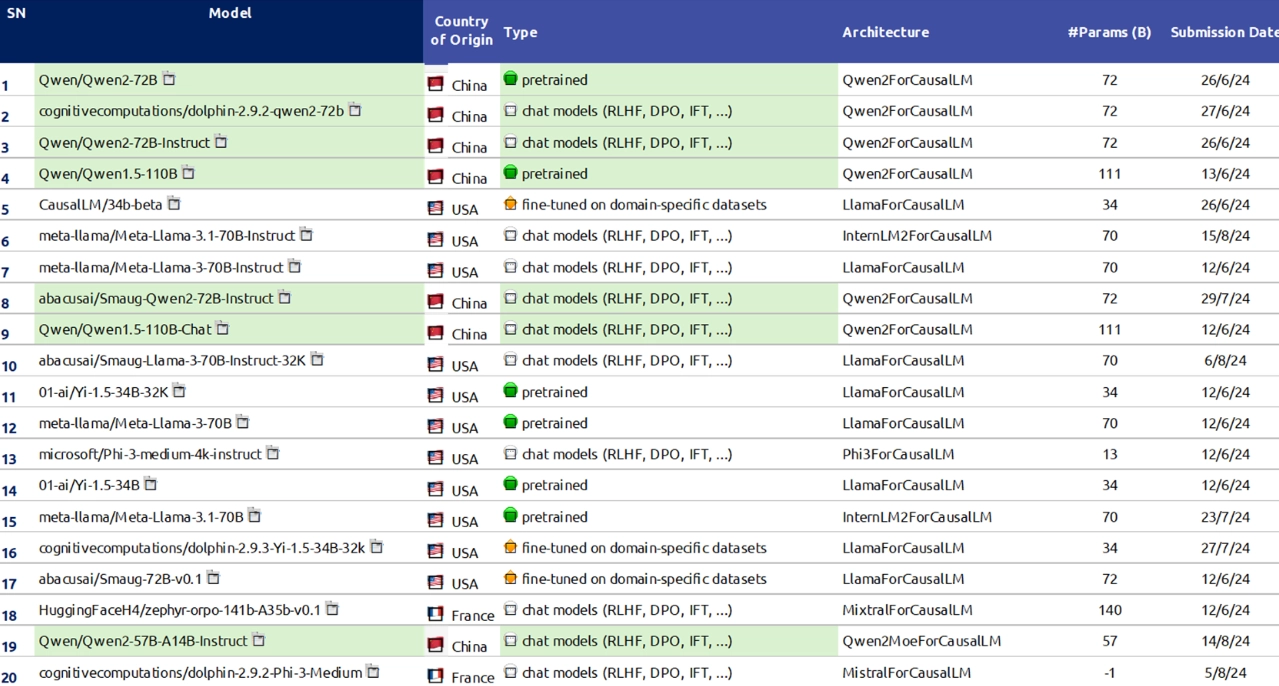

While the US is the clear leader in the source of top AI models, China dominates AI patents. In 2022, China’s patenting activities significantly outstripped the US, accounting for 61% of global AI patent origins compared to US’ 21% (Stanford Institute for Human-Centered Artificial Intelligence (HAI), 2023). Notably, in Hugging Face’s second leaderboard that ranks open LLMs against more challenging variety of tasks, Alibaba’s 千问 (Qianwen) models featured prominently among the top-ranked open models on Hugging Face leaderboard.

The notion of AI leadership being confined to the West is misplaced. China’s rapid development and official approval of adoption of LLMs, urging both citizens and enterprises to embrace AI on a large scale, highlights the prospect that China will continue to be a hotbed for many AI innovations to come and can provide businesses and governments with meaningful alternative AI solutions.

Figure 7. Hugging Face leaderboard of top-ranked open LLMs. The ranking is by the Massive Multitask Language Understanding Pro (MMLU-PRO) benchmark, which is used for evaluating the performance of LLMs on a broader and more challenging set of tasks compared to the original MMLU, designed to test the latest models’ capabilities in handling complex, real-world problems. Alibaba’s 千问 models (abbreviated as Qwen) is highlighted in green. (https://open-llm-leaderboard-blog.static.hf.space/dist/index.html)

Superficial integration: the reality of AI adoption

While the technology trends in AI are impressive, a closer examination reveals that many businesses are still engaging with AI at a superficial level. Despite the hype and the fear of missing out (FOMO), AI adoption often lacks depth, driven more by external pressures than by a deep, strategic understanding of how AI can transform operations. According to the 2024 Gartner Hype Cycle Report, “Generative AI is sliding into the trough of disillusionment” (Mearian, 2024).

8. FOMO is catching on

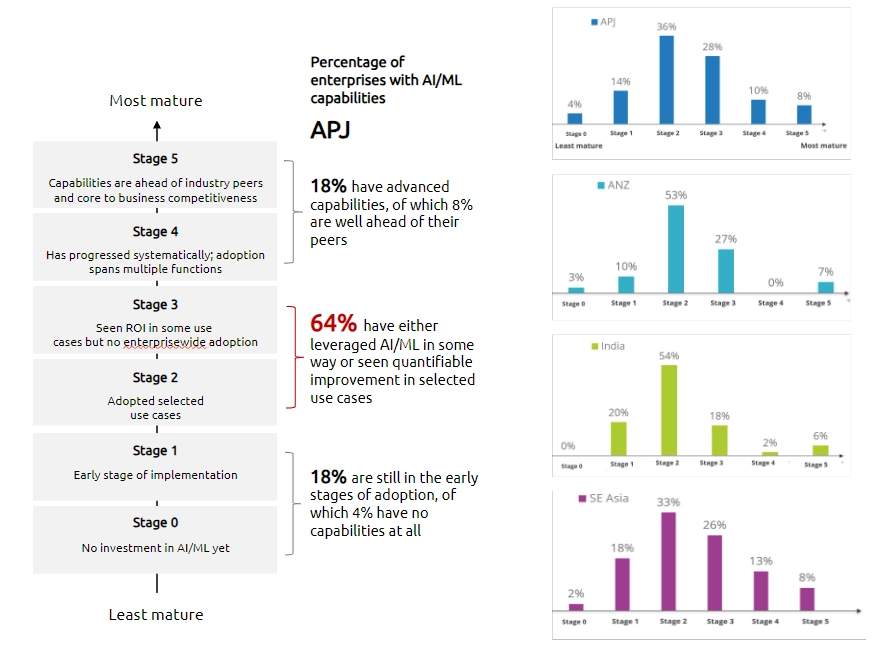

A recent survey by IDC reveals that in the Asia-Pacific region, only 4% of respondents have yet to introduce AI into their operations (Figure 7). This widespread interest in AI is not surprising, given the impressive technological advancements and the continuous hype from technology vendors. Additionally, national initiatives like Singapore’s National AI Strategy 2.0 are fuelling this momentum, encouraging businesses to adopt AI to enhance competitiveness across industries.

Figure 8. AI maturity in APJ organisations. IDC survey in 2023 shows that the majority of surveyed organisations (82%) are still in early stages of harnessing AI, and have not achieved scaled impact yet. Only a small percentage (4%) have not done anything and are yet to respond to recent advances in AI technology.

9. Reality check

However, as businesses wade into the AI era, they are starting to encounter challenges that temper their enthusiasm. Usability, safety, and enterprise readiness have surfaced as significant concerns. Many AI systems, while powerful, are not yet fully equipped to handle the complexities of real-world applications. This has made businesses more cautious about which use cases to pursue and how deeply to integrate AI into their operations.

Moreover, the lack of skilled personnel to manage and interpret AI systems often leads to suboptimal outcomes. Without the necessary expertise, businesses struggle to fully harness AI’s capabilities, resulting in implementations that fall short of expectations. Their use of AI tends to be experimental in nature, or in localised production systems for specific narrow parts of the business.

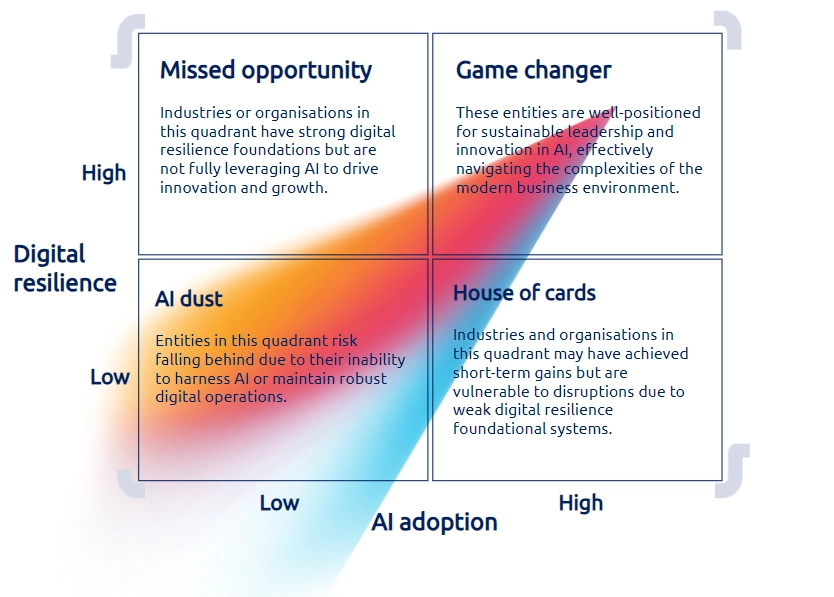

This state of “AI dust” can be overcome. To fully harness the potential of AI, companies must not only have a well-thought AI adoption strategy that factors in talent and ethics, they must also build the corresponding digital resilience. In other words, they will need a holistic approach of getting IT systems and digital platforms (which host the AI systems) to be ready for the AI era. This holistic approach can be visualised in an AI+DR Impact Matrix (Figure 8), which provides a practical framework to assess an organisation’s readiness in AI and digital resilience (DR).

Figure 9. AI+DR matrix. Organisations can use the AI+DR Impact Matrix to engage in strategy discussions, identifying gaps, and prioritising areas for investment not just in AI but also in DR. The matrix serves as a strategic reminder to ensure that as AI adoption increases, corresponding investments in digital resilience are made to maintain stability and security. (NCS, 2024).

10. Regulation rising

As AI technologies become more pervasive, so do concerns around their misuse and potential for abuse. Geopolitical tensions and ethical considerations are driving the development of regulatory measures aimed at controlling the deployment and impact of AI. These regulations, while necessary, add another layer of complexity for businesses trying to navigate the AI landscape. Companies, particularly multinationals, must now consider not only the technical and operational aspects of AI adoption but also the legal and ethical frameworks that govern its use in the markets they operate in.

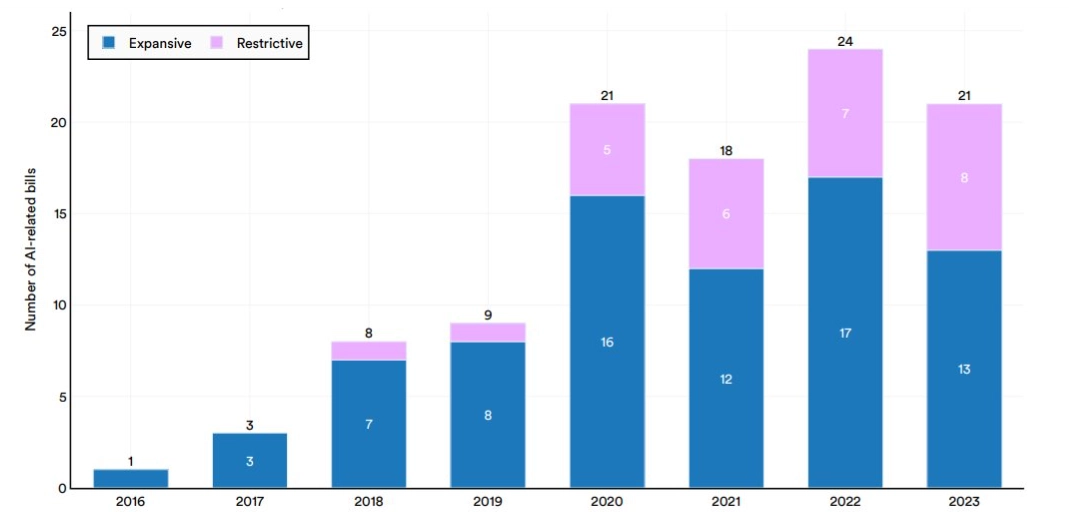

Not all the AI regulations enacted by countries are restrictive in nature, as shown in Figure 9. In Singapore, the Government has elected to adopt a “twin engine approach to AI regulation” (Yeong, 2024). Rather than implementing broad, sweeping regulations at this time, they have decided to pursue a more balanced approach that equally prioritises the adoption of AI technology and the safeguarding of consumer interests.

Regardless, the rise of AI regulation reflects the growing recognition that AI’s influence extends far beyond business operations, impacting society at large. As governments and regulatory bodies introduce new rules and guidelines, businesses will need to adapt quickly to ensure compliance, which could further slow the pace of deep, meaningful AI adoption.

Figure 10. The number of AI-related bills passed into law has seen a dramatic increase since 2019 in the countries studied by Stanford Institute for Human-Centered Artificial Intelligence (HAI) (2023), namely Andorra, Austria, Argentina, Belgium, France, Hungary, Italy, Kazakhstan, Luxembourg, Portugal, Russia, South Korea, Spain, United Kingdom and United States. Expansive bills enhance a nation’s AI capabilities while restrictive bills impose limitations on AI usage.

Conclusion

AI is undeniably pervasive, with rapid advancements in technology shaping the future of industries worldwide. From the emergence of powerful, multimodal models to the rise of open-source alternatives and retrieval augmented generation (RAG) systems, the state of AI technology is both impressive and evolving. However, despite these technological leaps, many businesses remain in the early stages of AI adoption, driven by fear of missing out rather than a strategic understanding of AI’s potential.

To truly harness AI’s transformative power, businesses must move beyond superficial implementation. This involves not only embracing the latest technological advancements but also developing a deep, strategic approach to AI integration. This means investing in sustainable, use-case-driven solutions, fostering the necessary skills within the organisation, aligning AI strategies with broader business goals, and navigating the increasingly complex regulatory landscape.

By addressing these challenges and seizing the opportunities presented by current AI technologies, companies can transition AI from a buzzword to a powerful driver of meaningful, lasting change across industries.

References

Ding, Y., Fan, W., Ning, L., Wang, S., Li, H., Yin, D., & Li, Q. (2024). A survey on rag meets llms: Towards retrieval-augmented large language models. . arXiv preprint arXiv:2405.06211.

Epoch AI. (n.d.). Data on Notable AI Model. Retrieved 24 August, 2024, from epochai.org.

Labonne, M. (25 July, 2024). I made the closed-source vs. open-weight models figure for this moment. Retrieved from https://x.com/ maximelabonne/status/1816008591934922915

Mearian, L. (22 Aug, 2024). Generative AI is sliding into the ‘trough of disillusionment’. Retrieved 26 Aug, 2024, from Computerworld: https://www.computerworld.com/article/3489912/generative-ai-is-sliding-into-the-trough-of-disillusionment.html

NCS. (11 July, 2024). the AI gambit: accelerate with digital resilience. Retrieved from ncs.co: https://ncs.co/en-sg/knowledge-centre/ articles/the-ai-gambit/

Precedence Research. (July, 2023). GPU Market Size, Share, and Trends 2024 to 2034. Retrieved 26 Aug, 2024, from precedenceresearch.com: https://www.precedenceresearch.com/graphic-processing-unit-market

Stanford Institute for Human-Centered Artificial Intelligence (HAI). (2023). AI Index Report 2023. Stanford University. Retrieved from https://aiindex.stanford.edu/report/

Tremayne-Pengelly, A. (6 6, 2024). Nvidia’s Market Cap Surpasses $3T: Here Are the Largest Buyers of Its A.I. Chips. Retrieved 26 08, 2024, from Observer.com: https://observer.com/2024/06/nvidia-largest-ai-chip-customers/#:~:text=Microsoft%20reportedly%20 plans%20to%20amass,during%20the%20same%20time%20frame.

Yeong, Z. (26 August, 2024). Singapore’s twin engine approach to AI regulation. Retrieved 26 August, 2024, from Straits Times Interactive: https://www.straitstimes.com/opinion/singapore-s-twin-engine-approach-to-ai-regulation